Nonprofit Resources

One Big Beautiful Bill Act Changes That Will Impact Student Cash Flow

The One Big Beautiful Bill Act (OBBBA), signed into law in July 2025, contains several provisions that will affect student borrowing and cash flow at higher education institutions. Three changes—loan proration, the elimination of new Grad PLUS loans and decreased Parent PLUS loans, and new aggregate loan limits—take effect July 1, 2026.

Institutions should begin assessing how these changes may alter student affordability and payment patterns to the institution, which could result in delayed timing of cash flows. Early planning can help reduce disruption when the new rules take effect.

Below is a summary of what is changing, along with illustrative examples showing how student costs may shift under the new law.

Loan Proration

Beginning July 1, 2026, federal student loans must be prorated for enrollment levels between half-time and full-time. While the U.S. Department of Education (ED) has not yet detailed the proration methodology, and may not do so until closer to the implementation date, we anticipate that students enrolled less than full-time will not be eligible for the full amount of loan funding.

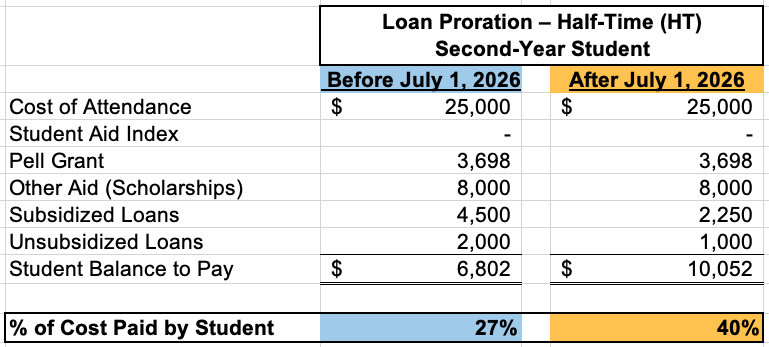

This could affect students’ ability to pay, leading to higher outstanding student account balances and additional pressure on cash flow. As an example, here is the potential impact of this change on a hypothetical undergraduate dependent student who is less than full-time:

The new requirements result in a 13% increase in the amount this dependent student would need to pay upfront. The cost would be even higher for an independent student.

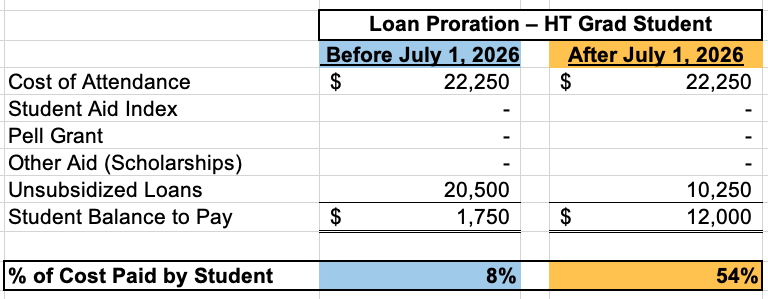

Here’s an example of the possible impact on a graduate student who is less than full-time:

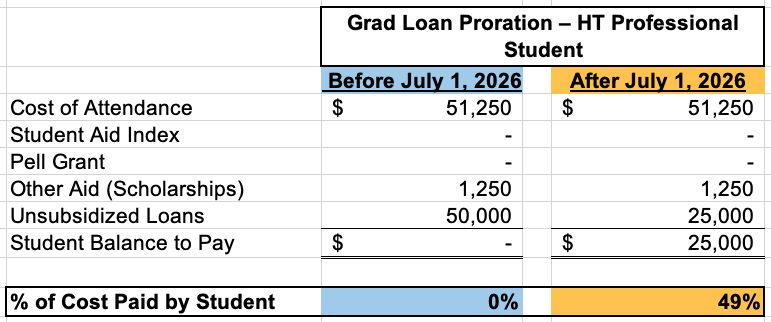

This student will see a large increase in the amount they will need to pay. Now let’s look at an example of a professional graduate student who is less than full-time:

As you can see, the impact could be substantial. While there are still unknowns about how ED will prorate the loans (such as by half-time/full-time status or by enrollment intensity, as with Pell Grants), it is important to be aware of this coming change and start considering how you will address it.

Elimination of New Grad PLUS Loans and Reduced Parent PLUS Availability

Under the OBBBA, students entering graduate programs who do not have a direct loan (Direct Unsubsidized or Grad PLUS) disbursed before July 1, 2026, will no longer be able to obtain a Grad PLUS loan. Students who are already enrolled in graduate programs and have direct loans can still borrow to complete their programs. The new deadline is three years or when the degree is complete, whichever comes first.

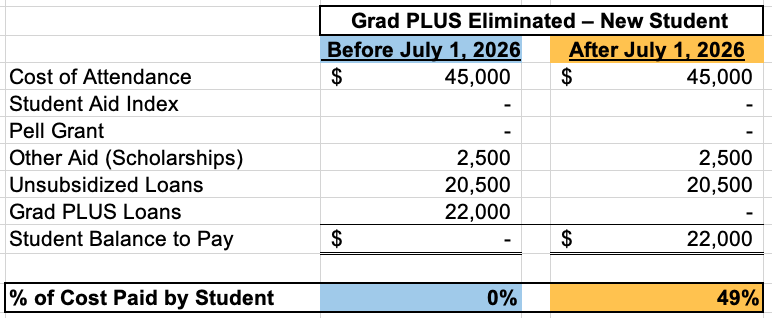

Here is an example of the impact on a hypothetical new full-time graduate student:

After July 1, 2026, the student will need to cover a large balance.

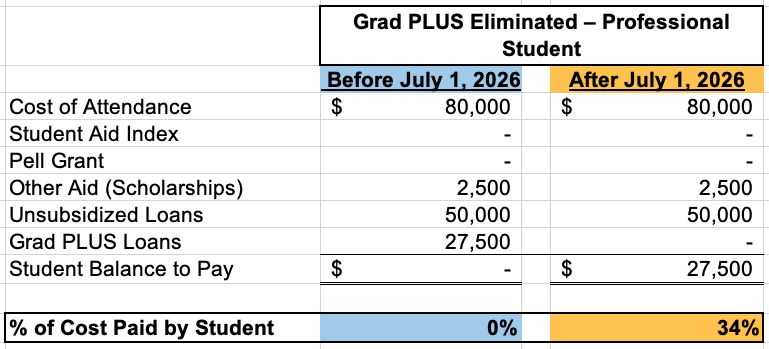

For a new full-time professional graduate student, the potential impact could look like this:

The financial burden increases as graduate programs become more expensive, especially if students are taking them part-time.

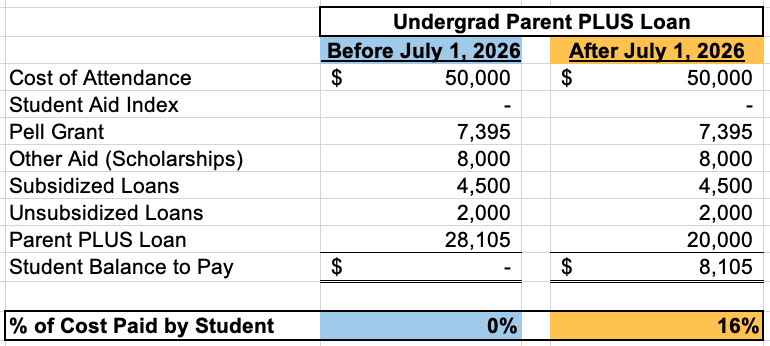

Additionally, Parent PLUS loans for undergraduate students will be capped at $20,000. Previously, parents could borrow up to the cost of attendance. Here’s an example of how this could affect the cost paid by an undergraduate student:

The cost the student pays will rise significantly after this change.

Aggregate Loan Limits

Undergraduate student loan limits remain the same under the new law, except for Parent PLUS loans. As of July 1, 2026, Parent PLUS loans will have a limit of $20,000 per year with an aggregate limit of $65,000 total per dependent student. Previously, students could borrow to cover the full cost of attendance, with no specific limits.

Under the OBBBA, graduate students will also now have an aggregate limit of $100,000 for direct unsubsidized loans, and professional students will have an aggregate limit of $200,000. Both types of graduate students will now have lifetime limits of $257,500. This flowchart from the National Association of Student Financial Aid Administrators summarizes the loan limits effective July 1, 2026.

Although the Federal Student Aid Office has confirmed that FAFSA updates will reflect these new limits, it is unclear how these changes will affect students who have already exceeded them.

Steps Institutions Can Take Now

To prepare for these changes, we recommend you consider:

- Updating your website for the 2026 – 2027 award year so students are aware of the coming changes when considering their financial aid packages.

- Indicating that financial aid packages are preliminary until official guidance is provided or July 1, 2026, whichever occurs first. The NASFAA website has checklists and other practice aids to help you coordinate and communicate this information to students.

Early, clear messaging may help manage expectations and minimize disruptions.

Another OBBBA Provision to Monitor: “Do No Harm” Accountability Metrics

Although the new “do no harm provision” of the OBBBA will not have an immediate effect, in its current form, it could impact the 2029 – 2030 award year.

This provision, which will replace the Fair Value Transparency/Gainful Employment framework, requires ED to consider how to evaluate undergraduate programs in which the median earnings of graduates are lower than the average earnings of high school graduates without degrees two years after graduation. Graduate program completers will be evaluated based on the median earnings of comparable bachelor’s degree holders. Programs that are not considered economically advantageous could lose Title IV eligibility.

For example, degrees awarded by a seminary that lead to pastoral ministry, Christian education, missions, or chaplaincy roles where the housing allowance is excluded from taxable wages reported on Form W-2, Box 1, would result in a lower income because this portion of the income is excluded from total wages. This could cause these programs to fail the single-earnings premium test when compared with national averages for all master’s graduates, many of whom don’t have a housing allowance, so the salaries used in the averages are higher.

An academic program is considered to have failed the test if two of the three consecutive award years display that:

- Failing programs represent either 50% or more of students with Title IV student financial aid, or

- 50% or more of Title IV revenues are derived from the failing programs.

Either situation could result in the institution losing eligibility for Title IV funds, including Federal Direct Student Loans, as in our seminary degree example above. This is just one example of a situation where the new measures set by the “do no harm” provision of the OBBBA might not reflect the underlying facts. See this article from the Higher Education Assistance Group for additional details.

Action Step: When the comment period for the provision opens, consider providing feedback for consideration by the Accountability in Higher Education and Access through Demand-driven Workforce Pell (AHEAD) Committee. We recommend that you watch the FSA Partner Connect Knowledge Center website for notifications about comment deadlines related to the AHEAD Committee agenda.

CapinCrouse is available to help with any questions as your institution works through these impending changes or other aspects of OBBBA implementation. Please contact us to learn more.

Additional Resource:

What Higher Education Institutions Need to Know About the One Big Beautiful Bill Act

Lisa R. Saul

Lisa serves as Principal and Uniform Guidance Director at CapinCrouse. She joined the firm in 1999 and has over 25 years of experience in performing and supervising Uniform Guidance audits* of Department of Education student financial aid programs and a variety of federal funding, as well as program audits and agreed-upon procedure engagements of various state-funded programs. Lisa oversees the firm’s more than 100 Uniform Guidance audits.