Nonprofit Resources

Revisiting the Accounting Standard for Leases: ASC 842

Although Financial Accounting Standards Board (FASB) ASC 842, Leases, has been effective for several years, many nonprofit organizations run into questions and challenges with its practical application. It’s important to revisit the basic principles to ensure leases are correctly captured in your organization’s financial statements.

This step-by-step guide revisits the core decisions required under ASC 842, addresses common implementation questions, and offers practical clarification to help you record leases accurately.

In this article, you’ll learn how to:

- Identify whether a contract contains a lease

- Determine which payments belong in your lease calculations

- Establish lease terms and appropriate discount rates

- Classify, measure, and account for leases throughout their life cycle

We also share a free resource to help you implement the lease standard efficiently and effectively.

Step 1: Determine if a Contract Contains a Lease

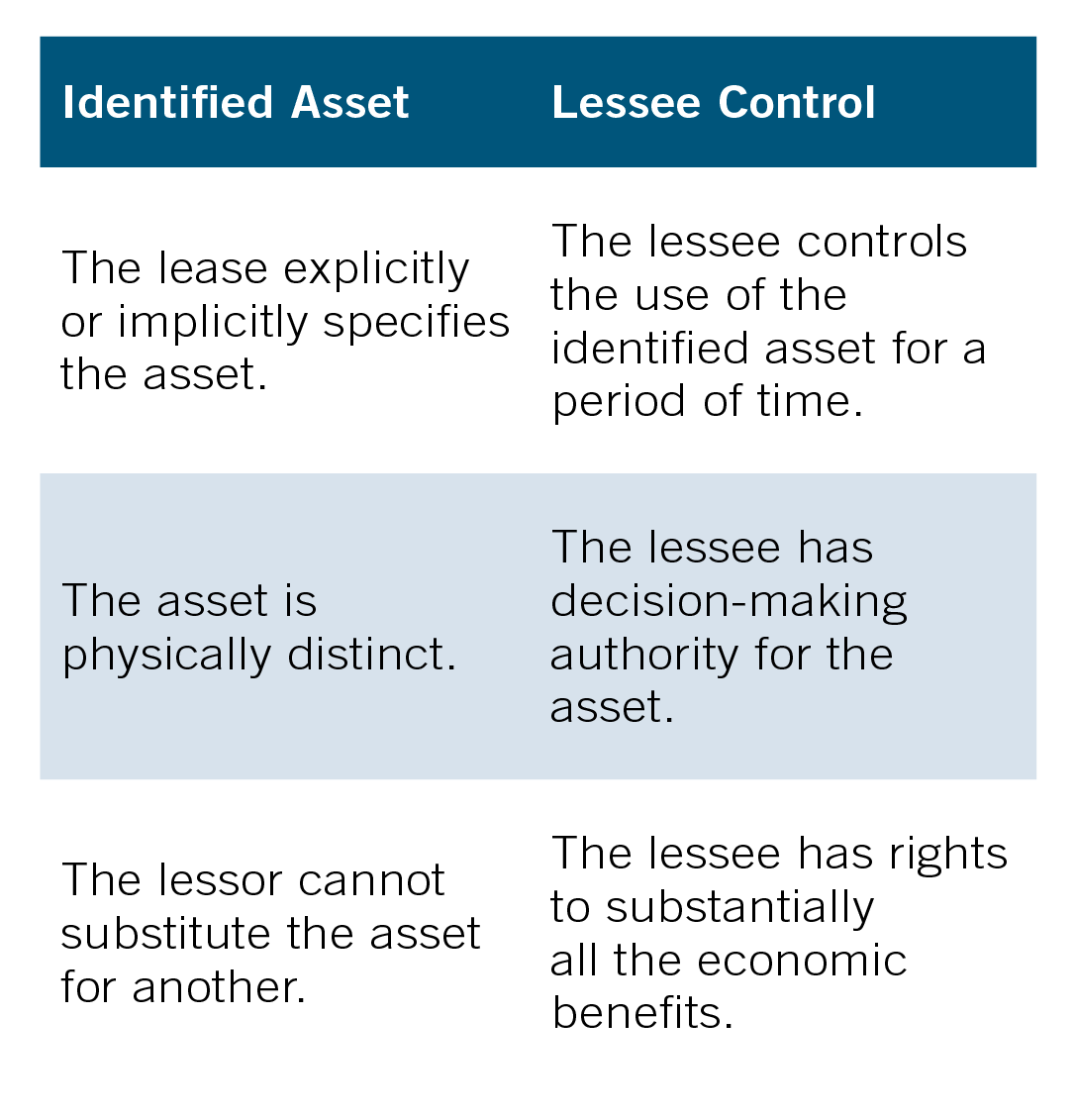

Under ASC 842, the definition of a lease includes a contract (or part of a contract) that conveys the right to control the use of an identified asset for a period of time in exchange for consideration. This definition is clarified to focus on two areas:

- Whether there is a specifically identifiable asset

- Whether the lessee has control of the asset

Here are examples of an identified asset and lessee control:

If there is no specifically identifiable asset, or if the lessee does not have control of that asset, the contract does not contain a lease, and the lease standard accounting would not apply.

If there is no specifically identifiable asset, or if the lessee does not have control of that asset, the contract does not contain a lease, and the lease standard accounting would not apply.

Q: What if the contract isn’t for consecutive periods of time? For example, a church has a contract to lease a building only on Sundays from 7 a.m. to 1 p.m. Has enough time elapsed between Sundays that the lessee wouldn’t have control of the asset?

A: No. The evaluation of control is based on the specified time periods in the contract, even if they are nonconsecutive. In this example, you would look at the elements of control in the chart above as related to the periods of time listed in the contract.

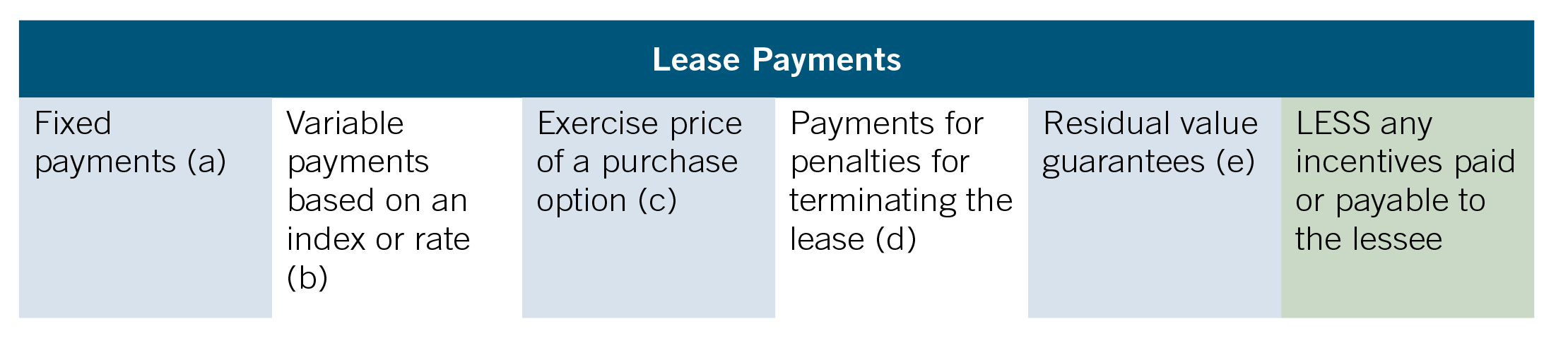

Step 2: Determine Which Payments are Considered Part of the Lease Calculations

There are two key components to determining which payments are included in the lease calculations. You need to know:

- Which payments are included within the lease calculations, and

- The portion of the consideration paid that is attributable to the underlying lease and nonlease components

(a) Includes payments made by the organization prior to the lease term.

(a) Includes payments made by the organization prior to the lease term.

(b) Variable payments that depend on an index or rate are calculated based on the rate at the inception of the lease. The organization excludes variable payments that are not based on an index or rate from consideration; these are expensed in the period they are incurred.

(c) Include only if reasonably certain that the organization will exercise.

(d) Include only if the lease term reflects the lessee exercising an option to terminate the lease.

(e) Include the amount that is probable a lessee will owe under residual value guarantees.

Once you know what types of payments are included within the calculation, you then need to know the portion attributable to each of the underlying lease and nonlease components.

Components are items or activities that transfer a good or service to the lessee. Lease components are paying for the right to use the asset; nonlease components are paying for other goods or services not related to the asset. Some leases have a single component, while others may have multiple components. For example, a copier lease may have two components: a lease for a specific asset, and ongoing maintenance of the copier. Identifying these separate components is key to ensuring calculations are made correctly.

Organizations may make an accounting policy election to treat all lease and nonlease components as a single lease component. (The election can be made by the underlying class of asset, such as equipment leases, for example.) This means that allocating the current lease payment across the different components is unnecessary. However, choosing this election would result in a higher right-of-use asset and liability on your books.

Q: An organization receives the use of rental space without consideration being paid. Is this transaction still captured under the lease standard?

A: No. If no consideration is exchanged, the lease is accounted for under contribution guidance (ASC 958-605), not under lease guidance. However, if rent-free periods are followed by periods during which consideration exchanged, this would fall under the lease standard.

Q: The contract for office space includes taxes and insurance as part of the consideration paid. If an organization elects to treat all components as a single lease component, are these costs included in the payments used for the lease calculation?

A: It depends. If the taxes and insurance costs are a fixed cost to the lessee (a gross lease), the payments associated with these costs are part of the “consideration in the contract” and affect the measurements of the lease assets and liabilities. If the costs are variable (a net lease), they are excluded from the lease payment calculation and treated like any other expensed period cost.

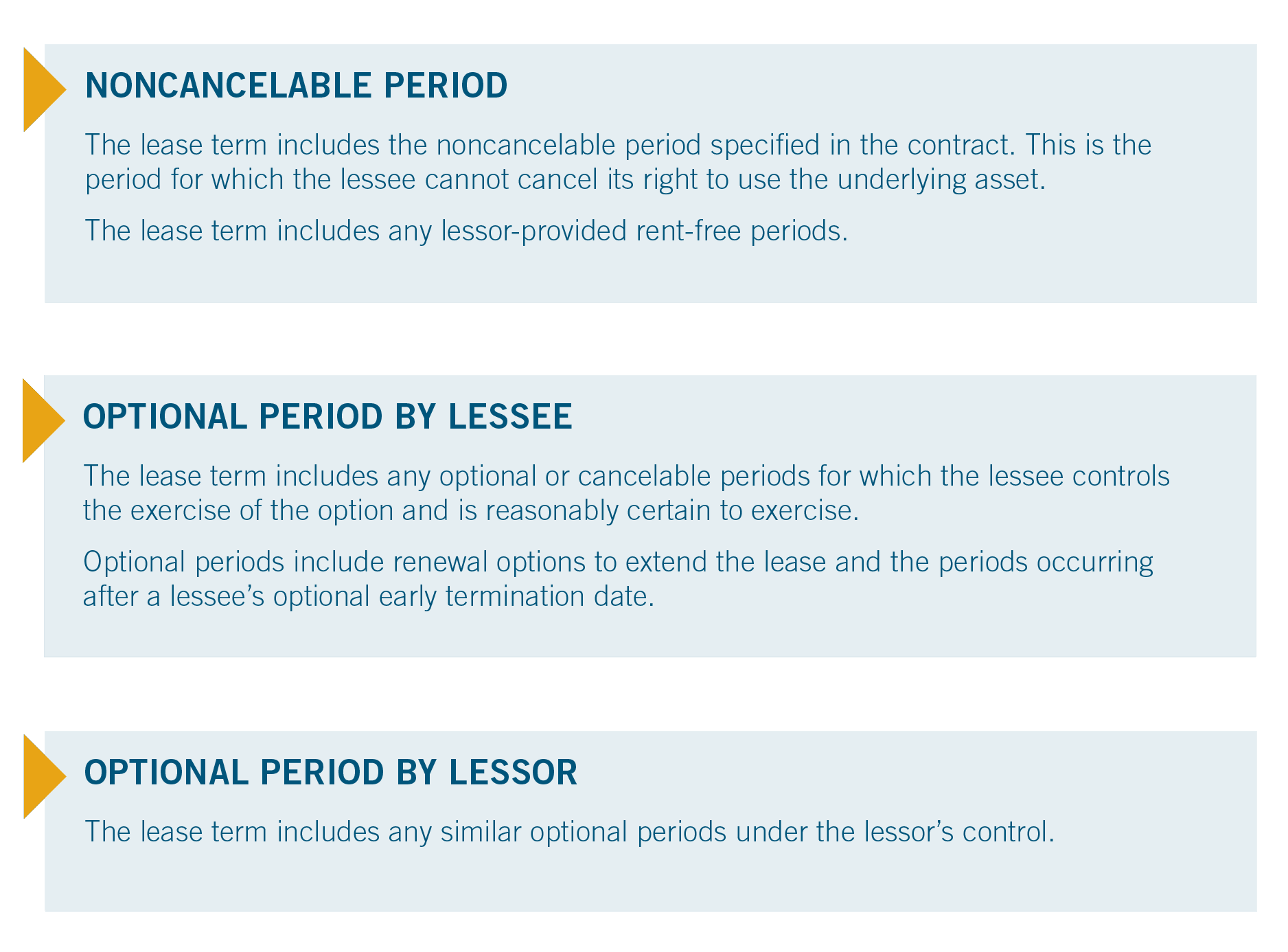

Step 3: Determine the Lease Term

The lease term begins on the commencement date and always includes the contract’s noncancelable period, including any rent-free periods. The noncancelable period is the period during which the contract is enforceable, and both parties therefore have rights and obligations to continue the lease. A lease is no longer enforceable when both parties have the unilateral right to terminate it without the other party’s permission, with no significant penalty.

If the contract includes an option for you to extend the term of the lease, include all periods your organization is reasonably certain to extend in the lease term.

Reasonably certain is a high threshold of probability that must be met to include the optional lease periods above in the lease term for the purpose of determining the lease standard calculation. Your organization should consider the relevant factors that create an economic incentive for you to exercise or not exercise an option, including contract-based, asset-based, entity-based, and market-based factors.

Consider these factors:

- Is the price of a lease renewal option at a fixed rate, or is it a discounted rate that creates an economic incentive for you to renew?

- Are there leasehold improvements that would make extending the lease term beneficial?

- Is the leased asset significant to your organization’s operations? If so, is there a readily available replacement asset?

- Do you have a sublease term that extends beyond the noncancelable period of the lease?

It’s important to note that management’s intent to renew a lease or its history of renewing similar arrangements does not directly correlate to concluding that the organization is reasonably certain to exercise an option. There still must be a compelling economic reason to renew.

If the contract includes periods that the lessor has the option to extend, you, as the lessee, must include these periods in the lease term. The likelihood of the lessor exercising the termination option is not considered in evaluating the potential impact on the lease term.

Q: A lease has an initial term of five years. However, the contract states that the lease may be canceled at any time with 90 days’ notice, for any reason. What is the noncancelable period for calculating lease assets and liabilities?

A: Assuming the organization’s cancellation can occur without incurring a more-than-insignificant penalty, until notice is given, the noncancelable period would be 90 days. However, if the penalty to the lessee would be more than insignificant, the noncancelable period may be longer than 90 days.

Examples of more-than-insignificant penalties include:

- Cash payments upon termination that are detrimental to the organization

- The leased asset is so central to the organization’s operations that termination would have a significant economic impact

Q: The lease standard seems like a lot of work. Are there any exemptions so we don’t have to record leases this way?

A: An organization can adopt the short-term lease exemption. This allows organizations with a lease that has a term of 12 months or less to exclude that lease from the calculations and record straight-line lease expense instead. Note that leases with a term of even just a few days greater than 12 months do not qualify for this exemption.

This exemption is determined at lease commencement by determining the lease term through the steps above. Leases that were previously recorded as right-of-use assets and liabilities and later have a term of less than 12 months do not qualify for this exemption.

Q: A written contract has no stated lease term. Instead, it states that consideration will be paid monthly as long as the lessee retains the right to use the asset. What is the lease term for this month-to-month lease?

A: The lease term for month-to-month leases is established in the same manner as for all other leases: by determining the noncancelable period, then the optional periods reasonably certain to be exercised by the lessee. In month-to-month leases, the noncancelable portion would be a month. If the organization is reasonably certain to exercise an option to renew for multiple months, those additional months would also be included in the lease term. Any optional periods under the lessor’s control also must be included in the lease term.

Q: Our organization has an existing lease with a related party that isn’t in writing. How do we determine the lease term when we don’t have a written document, just a handshake agreement?

A: We recommend organizations get these types of leases in writing. Lease terms with related parties under common control are determined on the basis of the legally enforceable terms and conditions of the lease. If it is just a handshake agreement, this becomes difficult.

The organization can adopt a practical expedient to use the written terms and conditions rather than enforceable rights and obligations. This practical expedient can be adopted on a lease-by-lease basis and makes the determination of the lease term much simpler.

Step 4: Determine the Discount Rate

Determining an accurate discount rate is a critical component of the lease liability calculation. The initial lease liability is calculated based on the present value of the remaining lease payments, determined using the discount rate established at lease commencement. The higher the discount rate, the lower the lease liability will be.

You must use the rate implicit in the lease if you can readily determine it. An implicit rate is considered readily determinable when all material inputs are themselves readily determinable by the lessee. Unless specifically stated in the lease agreement, it is generally unlikely that the implicit rate will be used.

If you are unable to readily determine the rate implicit in the lease, you must use your incremental borrowing rate unless you elect to use the risk-free discount rate. Make this election by class of underlying asset.

Your incremental borrowing rate is the rate of interest that a lessee would have to pay on a collateralized loan with similar terms in a similar economic environment. As a result, the incremental borrowing rate will not always equal the borrowing rate on your loans.

The risk-free rate should be determined using a period comparable to that of the lease term. Organizations typically use the U.S. Treasury yield at the date of lease commencement and select the term closest to the lease.

Q: Can we update the discount rate after commencement if interest rates change?

Answer: No. The discount rate should not be changed unless an official lease modification occurs.

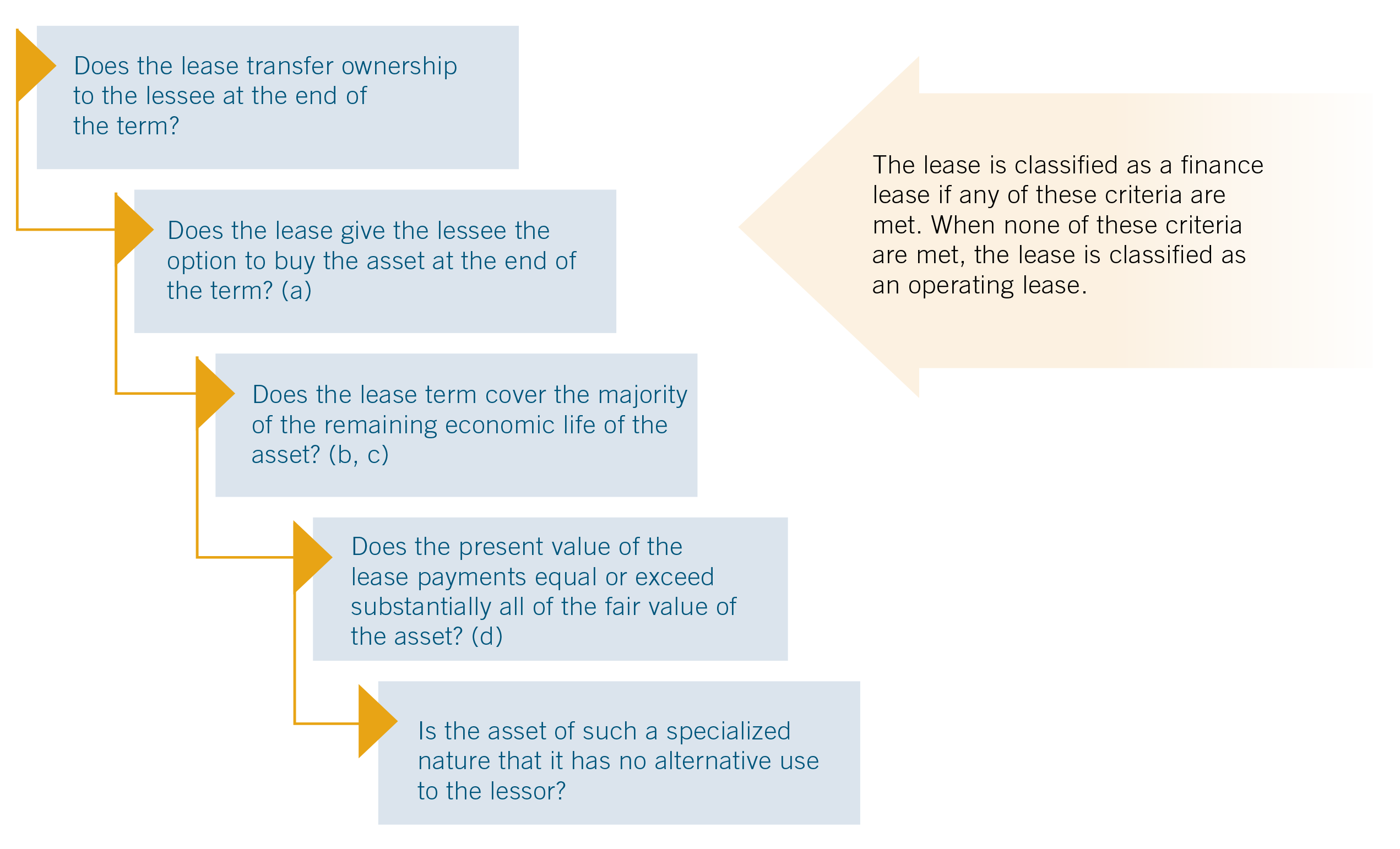

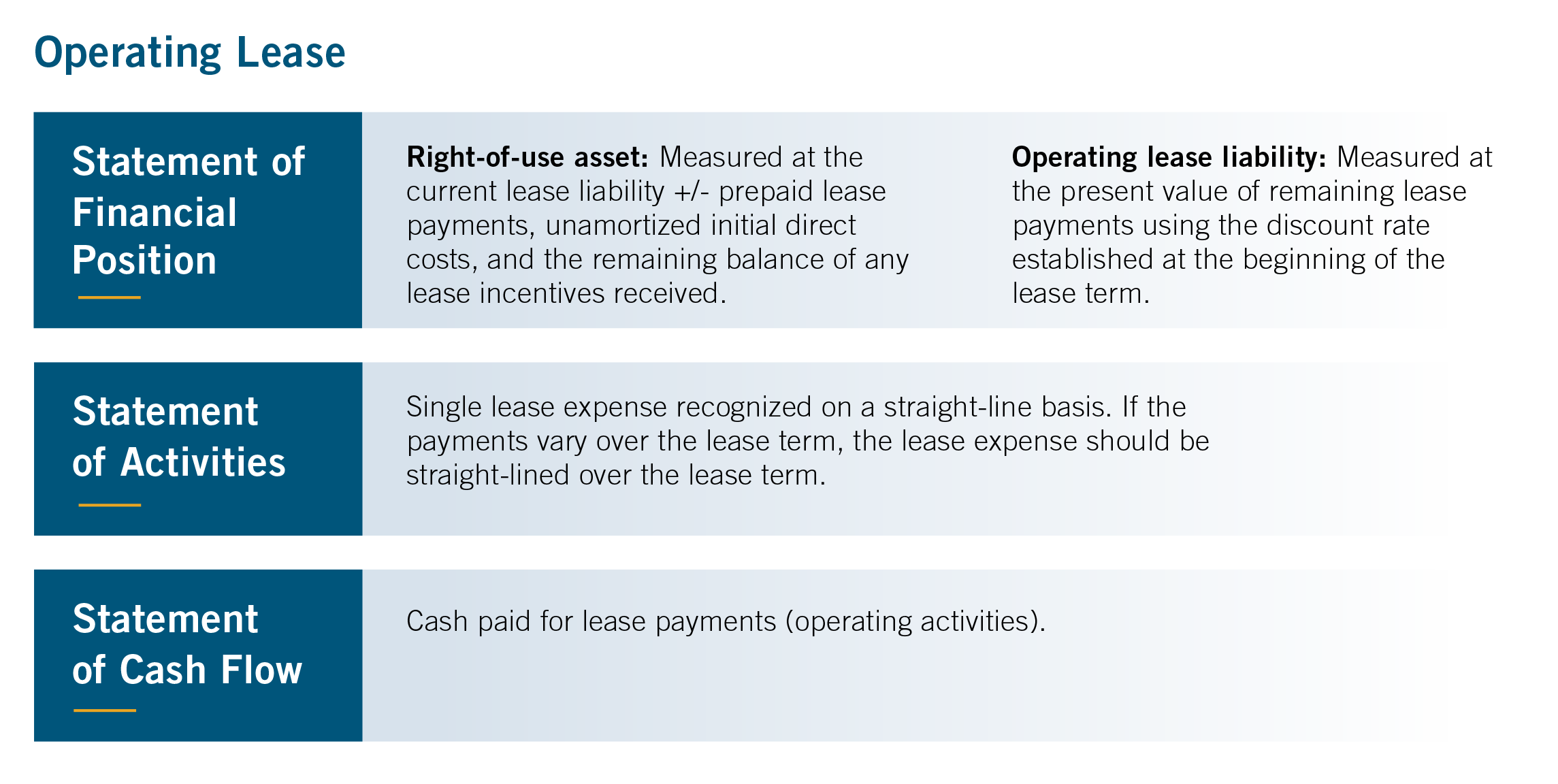

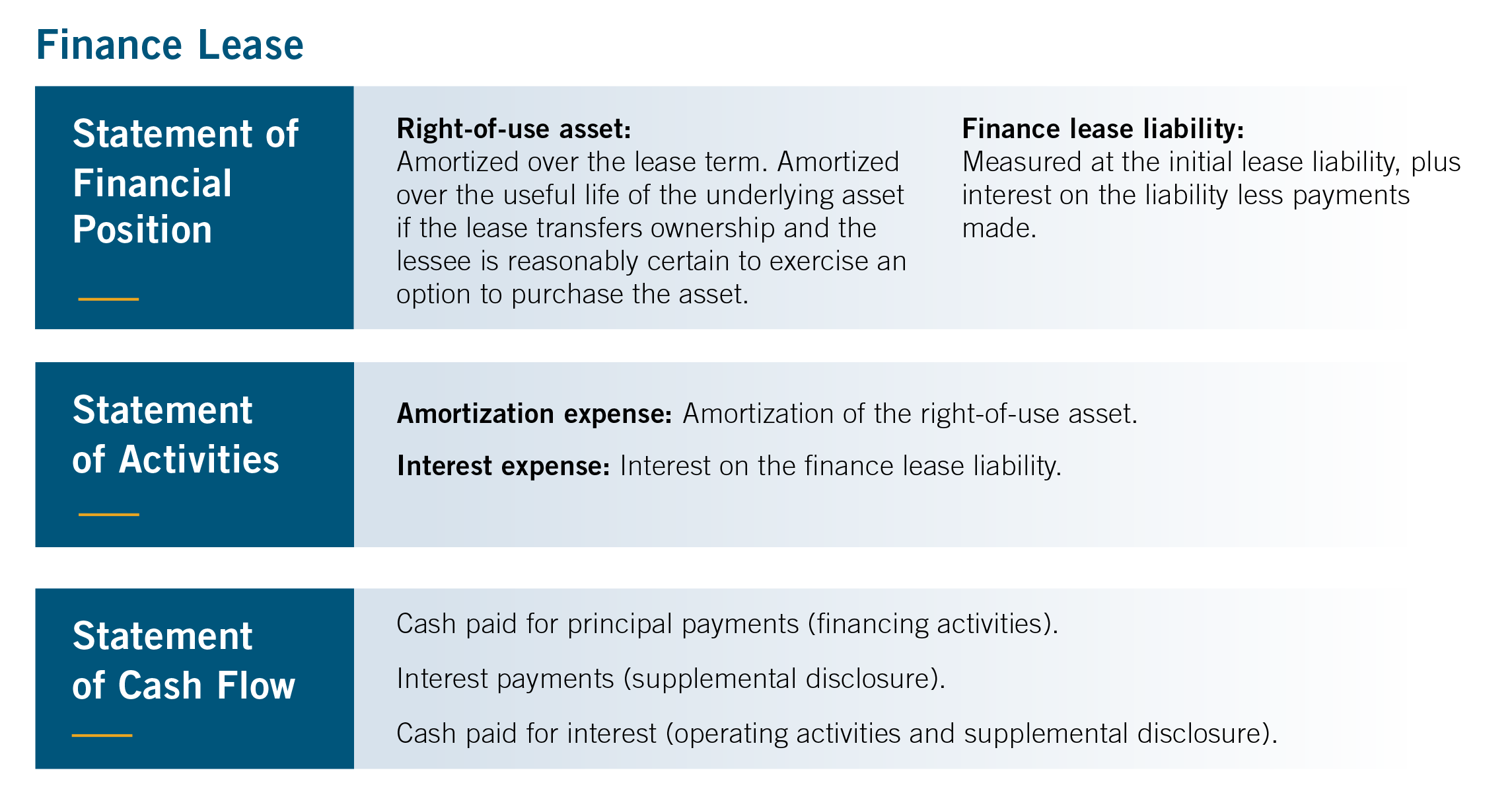

Step 5: Determine the Classification of a Lease

Lease classification is determined at the commencement date and affects the amount and timing of lease expense:

- Operating leases require lease expenses to be recognized on a straight-line basis over the lease term.

- Financing leases recognize interest expense and amortization expense, which generally results in higher expenses at the beginning of the lease that decrease over the lease term.

You can use this flowchart to determine classification:

(a) And the lessee is reasonably certain to exercise the right to buy.

(b) 75% or more of the remaining economic life of the underlying asset can be used to determine whether it is a major part of the remaining economic life of that underlying asset.

(c) If the commencement date falls at or near the end of the economic life of the underlying asset, this criterion shall not be used for purposes of classifying the lease. A commencement date that falls within the last 25% of the total economic life of the underlying asset can be used as a basis for determining whether the contract falls at or near the end of the economic life of the underlying asset at the commencement date.

(d) 90% or more of the fair value of the underlying asset can be used as a basis for determining whether it amounts to substantially all the fair value of the underlying asset.

Q: How do short-term leases affect classification?

A: If an organization adopts the short-term lease exemption, these leases are not recorded as a right-of-use asset or liability and therefore do not qualify as an operating or financing lease.

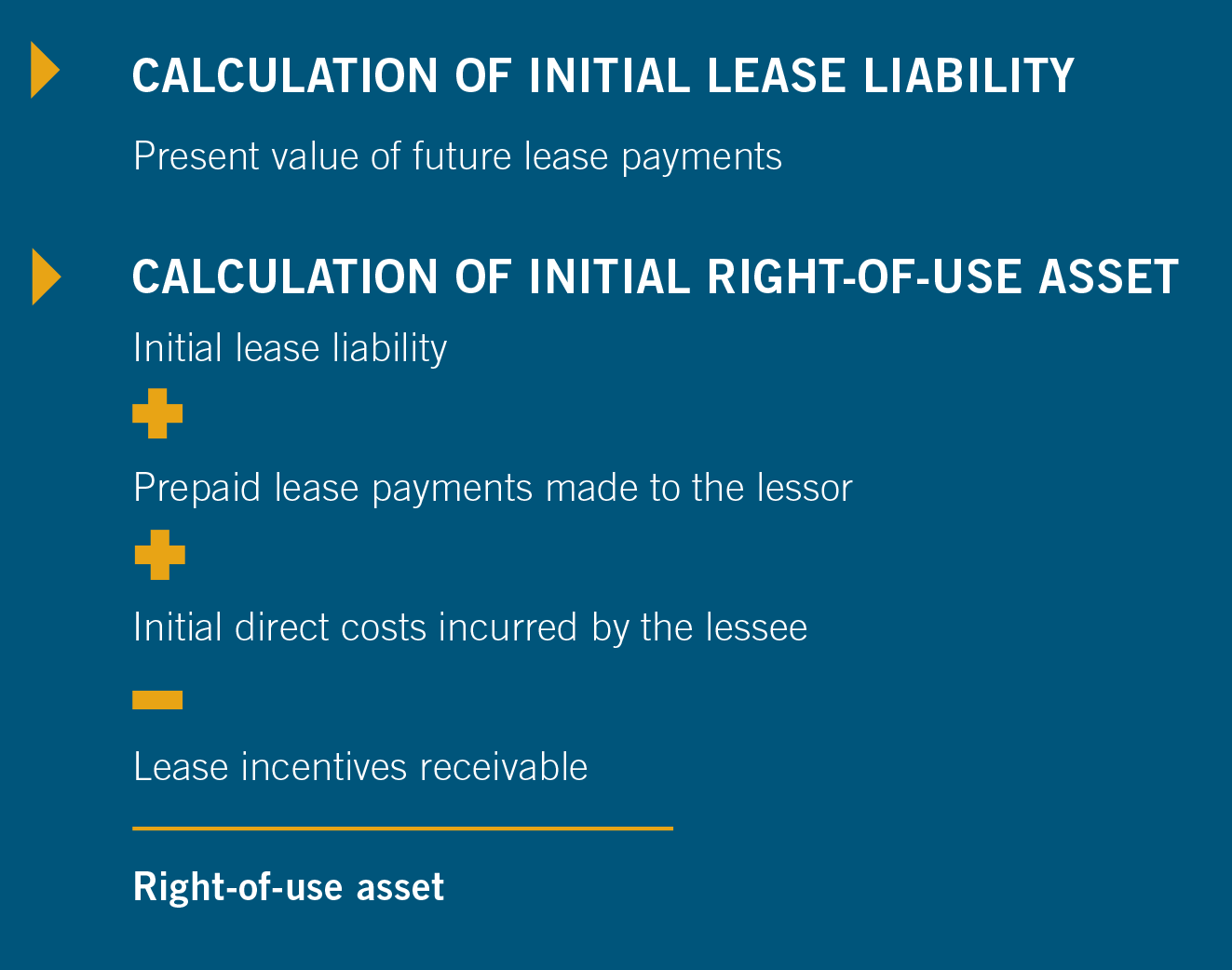

Step 6: Determine the Calculations for Recognition and Initial Measurement

If you’ve been following the steps above, at this point you will have determined:

- Whether the contract contains a lease

- Which payments are considered part of the lease standard calculation

- The lease term

- The discount rate

- The classification of the lease

Now you’re ready to make the initial calculation. Recognition and measurement of a lease occur at the lease commencement date, which is the date the lessor makes the asset available for use by the lessee.

The lease asset will be equal to the lease liability at the start of the lease, adjusted for any prepaid rent, initial direct costs, and lease incentives. The initial right-of-use asset and lease liability will be the same for operating leases and finance leases.

Q: An organization has a rental agreement in which the lessor agreed to pay $15,000 in tenant improvements. How is this captured within the calculation?

A: Tenant improvements reduce the right-of-use asset upon the initial calculation.

Step 7: Determine the Ongoing (or Subsequent) Measurement

Once you’ve completed the initial measurement of the right-of-use asset and liability, you must determine the necessary entries to accurately capture the subsequent measurement of the lease.

Finance leases will result in greater expense in the early years of the lease term and a lesser expense in the later years. Conversely, operating leases will result in a single straight-line lease expense throughout the lease term, unless another pattern is more representative of the lessee’s anticipated consumption of the asset’s future economic benefits.

From Implementation to Ongoing Compliance

After completing these steps, you will have successfully navigated through the key decisions that affect the accounting for each of your lease contracts and completed the initial and subsequent measurements based on those decisions and the underlying contracts.

Please do not hesitate to contact us with questions or to discuss how CapinCrouse can assist your organization with implementing ASC 842.

Free Resource: CapinCrouse Lease Toolkit

To support organizations navigating ASC 842, we developed a free Lease Toolkit designed to simplify implementation and compliance. The Lease Toolkit includes:

- A Key Lease Decision Reference Guide

- A Lease Information Gathering Form to streamline data collection

- A Lease Calculation Tool to assist with accurate calculations

Whether you are implementing ASC 842 for the first time or refining existing processes, these resources can help you apply the standard efficiently and with confidence.

Download the CapinCrouse Lease Toolkit >

Tammara Williamson

Tammara serves as Partner, CRI Advisors, LLC†, Partner, CRI Capin Crouse Advisors, LLC†, and Partner, Capin Crouse, LLC*. She joined CapinCrouse in October 2010. As a partner in the Colorado Springs office serving the firm's West region, she provides various assurance services to numerous types of nonprofit organizations, including churches, camping ministries, and international and mission-sending organizations. Tammara also serves as Director of Training within CapinCrouse.