Nonprofit Resources

Adopting CECL: What Nonprofits Need to Know

The Current Expected Credit Loss (CECL) standard requires nonprofits to estimate credit losses over the expected life of certain financial assets, including accounts receivable and loans receivable. CECL is a shift from an incurred-loss model to a forward-looking approach incorporating historical experience, current conditions, and reasonable and supportable forecasts. Nonprofit financial leaders should understand the scope, methodology changes, documentation requirements, and implications for financial statements.

Below are answers to FAQs about CECL for nonprofits, along with key insights for nonprofit organizations as they implement the standard.

What is CECL and Why Does it Matter for Nonprofits?

CECL is a Financial Accounting Standards Board (FASB) standard that changes how nonprofit organizations recognize and measure expected credit losses on certain financial assets.

CECL is the acronym for current expected credit losses, the overarching concept of the new FASB Accounting Standards Codification (ASC). Prior guidance was based on the incurred-loss model, which delayed recognition of credit losses until it was probable the loss had been incurred. Under CECL, organizations must estimate loss risk over the expected life of the financial asset and not just when the risk of loss is “probable.”

CECL was first introduced in FASB Accounting Standards Update (ASU) 2016-13, Financial Instruments – Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments. It is effective for all nonprofits for fiscal years beginning after December 15, 2022, including calendar years ending December 31, 2023, and fiscal years ending in 2024.

Does CECL Apply to All Nonprofit Organizations?

CECL applies to nonprofit organizations that have any assets within the scope of the standard. Broadly, the scope of CECL includes accounts receivable and loans receivable balances. Other financial instruments are included, as described in FASB ASC 326-20-15-2, but accounts receivable and loans receivable are the most common transaction classes applicable to nonprofits.

Notably, pledge receivable balances are not within the scope of CECL.

What is the Largest Shift in Methodology Under CECL? How Will That Impact Nonprofits’ Reserve Calculations?

The main methodology change is that CECL requires organizations to consider past events, current conditions, and reasonable and supportable forecasts to estimate loss risk over the expected life of the financial asset.

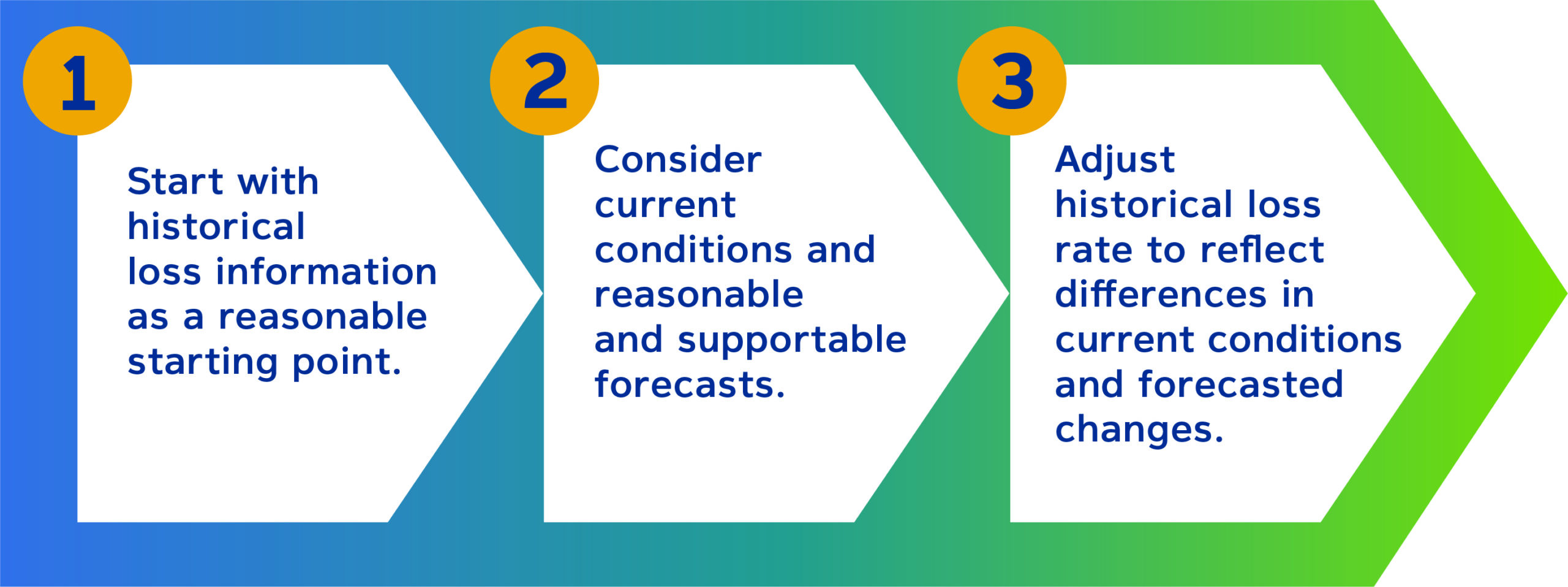

Nonprofits should take these steps to estimate the risk of loss:

- Consider their historical experience with the same type of receivables as a starting point

- Consider how conditions today differ from those of the past and what the future looks like

- Adjust the historical loss rate to reflect those differences

Do Nonprofits Need a New Methodology to Calculate Reserves?

Nonprofits can continue using their existing methodology, such as analyzing historical loss rates based on aging schedules, as a starting point for reserve calculations under CECL.

One change is that CECL requires organizations to pool assets with similar risk characteristics for reserve calculations. Any assets that do not share similar risk characteristics should be evaluated individually.

As an example, a university with a significant amount of traditional student accounts receivable plus accounts receivable from churches using its facilities for retreats may determine that these balances have different risk characteristics. Under CECL, the accounts receivable should be placed into two pools for evaluation.

How Should Nonprofits Calculate Reasonable and Supportable Forecasts Under CECL?

Nonprofits can develop reasonable and supportable forecasts under CECL by following four practical steps:

- Identify future conditions that would affect the risk of loss for each pool of receivables

- Evaluate what reasonably reliable forecast information is readily available

- Determine how far into the future forecasts can reliably be made

- Revert to historical loss information once reasonable and supportable forecasts can no longer be made

As a general guideline, most organizations forecast for up to two years. For accounts receivable due in less than one year, organizations are unlikely to revert to the historical loss period.

Determining a reasonable and supportable forecast does not require considering all available information sources. Instead, nonprofits can consider reasonably available, relevant information that can be obtained without undue cost and effort. This may include internal or external information, or both. For example, economic outlook information provided by an investment manager may be appropriate to include as a basis for forecasting.

What Are the Financial Statement and Disclosure Requirements Under CECL?

CECL introduces expanded financial statement disclosure requirements. The disclosures should enable a reader of the organization’s financial statements to understand:

- The credit risk inherent in the portfolio and how management monitors it

- Management’s estimate of expected credit losses

- Changes in the estimate during the reporting period

Each organization should assess the appropriate level of detail needed to meet the standard’s objective, based on the organization’s specific facts and circumstances. If too much aggregation is provided, important details may be missed. However, if organizations provide too much disaggregation and detail, material information could be obscured.

The required disclosures include:

- A description of management’s policy and methodology for developing the allowance for credit losses

- A roll-forward of changes in the allowance

- Transition disclosures in the year of adoption

- An aging analysis of past-due loans1

- Credit quality indicators1

If a balance is relatively immaterial to the overall financial statements, organizations may consider providing the disclosures above in narrative rather than tabular form.

The allowance must be presented on the face of the statement of financial position as:2

- A separate line item from the corresponding receivable balance; or

- Asset shown net of receivable, but with the amount disclosed in a parenthetical reference

What CECL Documentation Should Nonprofits Maintain?

Clear, organized documentation is essential. A nonprofit’s CECL documentation should include:

- The pools it will use to evaluate expected credit losses and how those pools were determined (ASC 326-20-30-8)

- The rationale for evaluating a receivable on an individual basis rather than with its respective pool

- What historical period of losses will be included in the analysis

- How current conditions differ from those of the historical period used

- What future forecasts impact the collectability of financial assets

- What period it can reasonably forecast and when it will revert to historical losses

Key Takeaways for Nonprofit Financial Leaders

CECL requires nonprofits to adopt a forward-looking approach to estimating expected credit losses while maintaining thorough documentation and consistent methodologies. Understanding which assets fall within the scope of the standard and planning for the impact on financial reporting is essential.

Please contact us with any questions or to discuss how CapinCrouse can assist you with CECL implementation.

1Disclosure not required for accounts receivable due in less than one year.

2Materiality can be considered for this requirement as well.

Lisa Wabby

Lisa serves as Partner, CRI Advisors, LLC †, Partner, CRI Capin Crouse Advisors, LLC†, and Partner, Capin Crouse, LLC*. She joined CapinCrouse in 2006 and has acquired a broad range of experience through serving a variety of clients within the nonprofit industry, including churches, colleges and universities, loan funds, foundations, international mission organizations, and voluntary health and welfare organizations. In addition to providing audit, accounting, and consulting services, Lisa leads the firm's Quality Assurance team. In this role, Lisa is an integral part of developing content for continuing professional education, developing strategies to implement new audit and accounting standards, and providing technical assistance to team members across the firm.